Is your charity trading? There are many organisations that, perhaps, would be unsure about how to answer this question.

Trading as a charity can be complex. Some charitable organisations do not necessarily recognise what they are doing could be deemed a ‘trading activity’.

Simply, trading is an exchange of goods or services for money. HM Revenue & Customs (HMRC) use certain ‘badges of trade’ to ascertain whether an activity should be deemed as such.

Where charities are concerned, it’s important to distinguish between primary purpose trading, and non-primary purpose trading.

Charity trading – is it in relation to your primary purpose?

Trading that is undertaken in the course of carrying out a primary purpose, or helping to achieve the aims and objectives of the charity is, as you might expect, ‘primary purpose trading’.

Examples might include a social care charity charging fees for the running of a care home, or a theatre charity selling tickets for a production.

It is also possible that some ‘ancillary’ trading will be viewed as furthering your charitable work and so deemed to be trading in relation to your primary purpose. This might be the provision of food and drink at a theatre café.

You will not be required to pay tax on any of the profits you receive from these activities.

Non-primary purpose trading

Non-primary purpose trading refers to trading that happens outside of your primary purpose. This is trading that does not directly contribute to your charitable objectives. Profits received from non-primary purpose trading are generally liable to Corporation Tax.

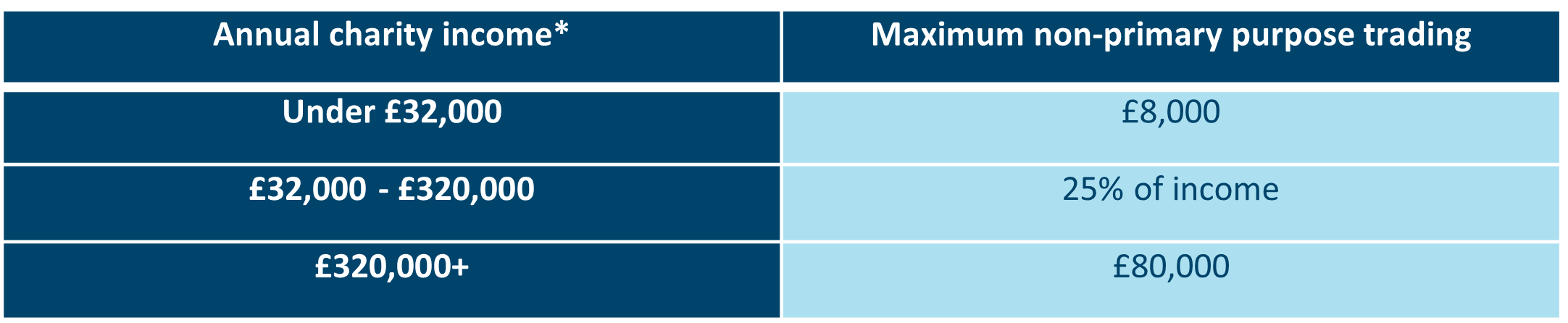

The ‘small-scale exemption’ for non-primary purpose trading

If your charity does undertake some non-primary purpose trading, there is a small-scale trading exemption that it is worth knowing about.

This exemption enables you to conduct non-primary purpose trading up to a certain turnover level, without attracting a tax charge. The thresholds are as follows:

*Annual charity income is your total income before deduction of expenses and tax. If thresholds are breached then all the profits from that trade become subject to tax.

Should we set up a trading subsidiary for our charity?

If your income from non-primary purpose trading regularly exceeds the small-scale trading threshold, or if the trading in question is considered particularly risky, you may want to consider whether a trading subsidiary is right for you.

A trading subsidiary would be wholly owned by the parent charity, and allowed to carry on a trade on behalf of the charity.

Worth noting is that some of the directors of the subsidiary should be independent of the parent charity. The relationship between the two entities should be kept at ‘arm’s length’.

Operating a trading subsidiary can help you to minimise the tax payable on trading activities, and to ring-fence your charity’s assets from any undue risk.

Trading subsidiaries can donate profits to the parent charity, as a Gift Aid donation. Charitable donations relief can then be claimed to reduce its Corporation Tax liability.

As for the parent charity, the receipt of Gift Aid donations is not taxable if the funds are used solely for charitable purposes.

Payments should be made as cash given to the charity, and within nine months of the end of the accounting period in which the profits were made.

VAT implications

The trading subsidiary will need to register for VAT if its vatable supplies exceed the current threshold (£85,000). However it can also benefit from some VAT reliefs available, allowing it to maximise on its fundraising.

The parent charity should also be careful; charges made to the trading subsidiary could see them breach the threshold as well.

A charity can choose to form a VAT group registration with its trading subsidiary in order to simplify administration of the tax, to minimise intra-company charges and to maximise recovery.

Trading subsidiary: Pros and cons

The decision about whether to establish a trading subsidiary for your charity is one that should not be taken lightly. We would encourage you to seek expert advice.

There are a number of important considerations, including but not limited to the following:

Pros

- Enables charity to carry out non-primary purpose trading, and to reduce liability to Corporation Tax on profits from these activities

- Commercial activity is ring-fenced, protecting the parent charity from risk and potential losses

- Can be beneficial where VAT is concerned

- Flexibility to operate in a way that the parent charity cannot – i.e., exploring more commercial activities

- Subsidiary has nine months after its accounting period end within which to donate profits to parent charity, and still claim relief

Cons

- Initial and ongoing costs associated with setting up a new company

- The ‘arms length’ relationship can be challenging to manage

- Not entitled to business rates relief

- Must have sufficient distributable reserves at the time the Gift Aid donation is made

Accountancy and advisory support for charities…

Our experienced partners and accountancy professionals are familiar with the regulatory requirements affecting charities. We understand the unique challenges impacting upon the sector, including the need to operate as efficient, cost-effective organisations.

Our proactive and practical advice is designed to help you find financial stability whilst also achieving your core objectives.

To find out more about the audit, accountancy, taxation and business advisory services that we offer to charities and not-for-profit organisations, contact our advisers in Cambridgeshire, Bedfordshire or Hertfordshire.